During these trying times, it’s very important that you are properly educated when it comes to protecting your credit report from future expensive credit repair!

Credit Reporting has become more complex since the introduction of Comprehensive Credit Reporting in 2014.

Although we didn’t see the changes for a while, we are now seeing most of the changes to our reports.

Changes include:

Your Credit Score

We all now have a credit score, ranging from -200 to 1200.

Our scores are based on our historical pattern of applications, current enquiries, our loan repayment history and any negative data, such as defaults and court actions.

Our scores are changing all the time and just one enquiry could pull your score down by 50 to 150 points.

Making sure you stay away from applying online and Payday type loans will help protect your score.

From the image above, you will also see a ‘VedaScore 1.1’.

This is the future score, or where the credit reporting agency believes our scores will sit in the next 12 months.

If this 1.1 score is very low, even if your current score is high, you could get knocked back for finance.

The future score depends on current type of credit sought and your current data, and your credit behavior.

Of course, at the moment, many people are suffering from the current global pandemic and are in need of finance.

Make sure you use a local accredited finance broker to research your Lender options before applying.

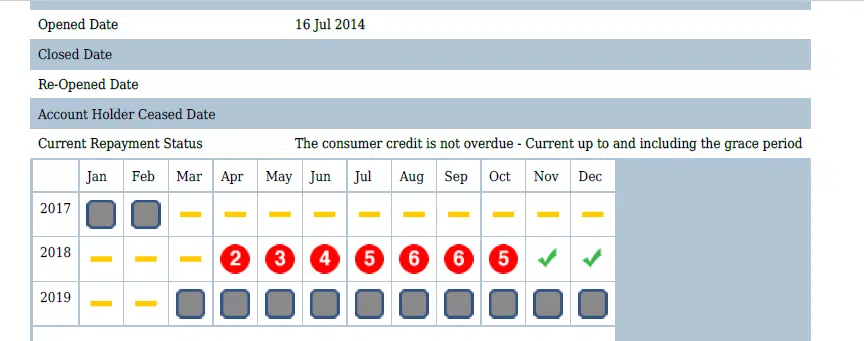

24-month Repayment History Information

In addition to our credit score, many Lenders are also reporting 24 months repayment history information.

You will see that each of your active loans are now recorded on your report.

– Noting if you have paid the loan on time every month.

This information goes back 24 months from today.

A ‘Zero’ is good, indicating zero arrears.

If you miss 1 months, the Lender will record a ‘1’ then a ‘2’ and so on until they finally list a default if you fail to pay for more than 60 days.

It’s crucial that you inform your Lenders if you are experiencing financial hardship.

This prevents them from recording negative repayment history information.

This may not affect you now…

But in a year’s time if you want to apply for a loan, it could stop you from getting the loan approval you need for your family or your business.

Make sure that you are contacting your Lenders in writing or on the phone to arrange financial assistance if you are suffering from financial hardship.

Lenders will then list a “R” for those months on their credit reports, whilst you are in the temporary financial assistance plan.

In the future, an “R” is not going to affect your credit score or ability to obtain finance.

Whereas if you don’t contact your credit providers now and are late on payments, you will have a “1” or “2” or “3” recorded on your repayment history information

This may cause problems in the coming months for you to obtain finance.

Lenders must provide temporary financial hardship, usually in the form of a 3 to 6 month freeze on repayments.

However, when the assistance package finishes, you will have to revert to normal payments.

If you see that there is incorrect repayment history information on your report, you can lodge a complaint to the Lender directly, email is always best, and they will run an investigation into the repayment history information, and amend it, if it is incorrect.

Usually the Lender will get back to you in around 30 to 45 business days.

As per legislation, this is how long Lenders have to reply to any written complaint or request.

Actively protecting our credit reports now will be vital as we struggle through the next few months with many Australians losing their jobs and needing financial assistance.

TOP TIPS

– Make sure you use a finance broker before applying online

– Complete a simple family budget update to make sure that you are covering your debts

– Be proactive and survive the war on corona.

This will greatly help you and your family when it comes to your future financial needs.

Should you have any questions on credit reports, Credit Fix Solutions can be contacted on 1300 43 65 69 or email [email protected]

We offer FREE credit reports, FREE credit report assessments, and No Result No Fee credit repair Australia wide.

DON”T get your report from free scoring websites – this is not your actual report and is NOT what the banks and lenders are looking at to assess you for finance.

Once you have your report, simply email it to us for your FREE assessment at [email protected].

OR call us today on 1300 43 65 69 and our scenarios team will get back to you.

3 Tips about Credit Repair you can’t afford to miss

Am I in need to repair my credit score?

This is the question that comes in our minds while thinking about credit repair.

And yes, a lot of us face the low credit score problems.

Dealing with such cases means that you are badly in need to fix your credit.

Just imagine yourself a few steps away from getting your utmost desire fulfilled like a dream car, a house, and many more but your low credit score is making you sick.

So, get your credit report fixed as soon as possible.

Now here are few awesome tips to raise your credit score.

1. Report all the disputed payment history

Firstly, you should remove all the disputed payment history. If it is a mistake at your end then clear your debt.

It can raise your score by a few hundred points.

Ask your creditor, if there is any disputed payment in your record.

2. Review your credit report

The review of a credit report is issued yearly, but you can get that on a request as well.

Review that report thoroughly and check your errors.

Check your mistakes that lead you to this ill repute.

This review can be very helpful in elaborating and eliminating all the errors.

3. Get guidance from a credit repair company

If you want an instant solution to fix your credit score, then get help from a credit repair company.

They provide you with the best promising solutions to repair your disputed credit score.

They assure scam free work where they operate as no result no fee.

There are thousands of fake companies that can steal your money for nothing, but you are the one to choose a trustworthy company.

Before choosing a company always keeps in mind their reputation and work quality.

A well-reputed company will always keep your satisfaction more prior.

At Credit Fix Solutions we offer No Result No Fee Credit Repair services Australia wide. No hidden application fees, and no upfront costs.

For more information, please email us at[email protected] or call us on 1300 43 65 69.

Many people think that bad credit holds them back from getting a job, obtaining low-rate loans and achieving a financial fit life. But the truth is that there is no sense in putting all the blames on your bad credit score. It is time to realize that it is not the credit score per se that bars you from achieving what you want in life, but your day-to-day decisions.

Here are some tips in eliminating the things that block you from making a progress in increasing your credit score and improving your finances:

Evaluate your spending habits

How you spend money is as important as how much you really have. Think about your income and the expenses that you have been making in the past 12 months. Are those expenses aligned with your goals? Are they equal or at least lower than your income? Your spending habits must be aligned with the results we want to achieve.

Let’s say, you are making $5000 a month and you make $2000 for repayments. That leaves you with $3000 to spend freely. If you are planning to increase your income, ask yourself if you are setting aside a certain amount of money to do that. Otherwise, you are simply making a plan but not doing anything to reach your goal.

Self-examination helps you think about your choices and the opportunities that could help you realize your goals and overcome bad credit. When your decisions are aligned to your goals, there is a better chance for you to get the results you wanted than simply waiting for your circumstances to get better before you take action.

Identify your financial goals

It is difficult to work on an unclear goal. Make up on your mind on what you really want to achieve. If the short-term goal is to increase the profits of your business, make sure to align all your management decisions into boosting your business revenues even if you need short term loans for business. Let’s say, you want to double your sales at the end of the month; don’t spend your loan proceeds on things which have no relation into boosting your profit margins. You can set aside other unrelated actions, and focus more on sales-related tactics such as improving product quality, increasing marketing efforts and improving customer service.

Know what you want to achieve is equally important as knowing what to do. By achieving clarity of purpose, you will minimize actions that could possibly stifle your progress. So, if you want to invest money on a particular endeavor, invest time in clarifying your goals. It will guide you not only in contemplating the results you wish to realize, but in implementing related strategies that could guarantee good results.

Eliminate expensive habits

Here are sneaky habits that are eating up your money:

Financial statements

Keeping track of your bills and receipts are a lot easier these days because most companies are going paperless. But, the obvious downside is that is also easier to overlook. So, it will be wise to check your financial statements regularly. Doing so, can help you check if there are recurring charges or incorrect entries that are sucking up your budget and damaging your credit score so that you can dispute them with your credit provider. If you are no longer using certain services, you can drop them altogether.

Wasting food

If you don’t have a weekly menu plan, it is difficult not to waste food. Unless of course, if you are feeding a bunch of teenagers inside the house, who love leftovers and anything inside the fridge. But, if you’re cooking for yourself or for two persons, make sure that you plan ahead of time. It will help you to stick to your menu’s ingredients every time you shop. It will keep you from overstocking canned goods and grocery items that you won’t consume anytime soon.

Stress shopping

How many times did you buy an item simply because you are stressed or you feel down? When we go to the mall to “feel better”, we may end up buying things which we don’t really need. It is similar to doing your grocery when you are really hungry. You may buy food items, like junk foods simply because you want to eat. So, next time that you want to relieve stress, go to places where you don’t have to do some stress shopping, like a park, your favorite gym or anywhere peaceful so you can relax.

Other expenses

If you are spending a lot of money on gym membership or an expensive hobby, maybe it is time to look for a cheaper alternative. Buying used sports gears or simply renting those items are way cheaper than actually buying brand new gears. There are also cheaper gyms that offer good services similar to what luxury gyms offer. If you can save money and enjoy the same quality of services, why not opt for the option that allows you to save more money in return?

Multiple factors contribute to falling into debt and straying from having a financially fit life. However, being mindful of all these factors will change your life for the better.

Editorial Note: Opinions expressed here are the author’s alone, the author being www.australianlendingcentre.com.au, and are not those of Credit Fix Solutions, any bank, credit card issuer, airline or hotel chain, and have not been reviewed, approved or otherwise endorsed by any of these entities.

Sick and Tired of Saving Money while paying a debt? Read This.

“Building wealth is a marathon, not a sprint. Discipline is the key ingredient.”

Most of the common New Year’s Resolution is to s be saving money.

But how can you save money if you are also in debt?

Use these straight to the point tips to come up with ideas to saving money in your day-to-day life.

Categorize your expenses

Amount of money you want to save

Cost of living (rent/loan, food and utilities)

Entertainment (travel, eating out, clothes)

From this, deduct the amount that you want to save from your income.

Noting how much you want to save.

You are more likely ending up spending a part of your saving so why not allot a few more dollars on top to offset the loss?

Once you’re done paying interest on your debt, you can put that money into your savings.

If you need assistance with a debt settlement, please call our friendly team on 1300 43 65 69 or email us at [email protected].

Set Your Goals

One of the most effective ways of saving money is setting a goal with a timeline.

Think of a motivation.

Want to buy a dream car in two years with a 20 percent down payment?

Now that you have a target goal, it will become easier for you to save each month.

Watch your savings grow

Check your progress every end of the month.

This will help you identify and fix problems quickly and start saving money.

It will also help you motivate yourself to stick to your plan and achieve your goal faster!

Eliminate unnecessary habits

Does smoking cost you $50 each week?

Do you buy snacks in the office for $10 every day?

That means you’re spending a $1,000 or more every year for cigarettes and junk food.

If you start eliminating these habits, imagine how much you can add to your saving account.

Step into a Debt-Free Life

Improving your savings while paying off your debt could be a challenge, but it does not mean it’s impossible.

You need to have a plan to successfully achieve both objectives.

The toughest part could be sticking to your budget, given your situation, which you must do anyway.

Remember that your financial behaviours can lead you to a road of financial freedom.

If you wish to be like our client who just had a saving of $13,905 reduced on her unsecured personal debts (names withheld for privacy), contact our friendly team now on 1300 43 65 69.

Email us at [email protected] or check out more articles at https://www.creditfixsolutions.co.nz/

“A budget is telling your money where to go instead of wondering where it went.”

A study shows that Australians rank third highest in the world when it comes to household debt. Source: http://www.businessinsider.com

There are two types of debt, a good one, and a bad one.

What is a good debt?

A good debt is a kind of debt which will benefit your wealth in the long run.

For example, a student loan to fulfil your college dreams, and an investment property loans which will allow you to earn income for renting and re-sell at a higher price.

What is a bad debt?

A bad debt is a debt where it decreases your wealth over a period.

This means, it can’t be used as an asset, and most of the time, you pay extra for the items that you can’t afford based on your salary.

The perfect example of this is using a credit card for unnecessary things, or to those that will diminish in value over time.

Whether you have a few hundred or many thousand owing on your credit card, below are some easy steps to start paying off the debt:

Figure out how much you owe

Collect all the credit card statements that you have.

Write it down or make a spreadsheet and list the balance and interest rate for each, you also want to know what your total amount of debt is.

Start a budget

Get organized. List down only the essential things that you need to buy in the grocery, followed by the bills you must pay and reduce your spending.

Does it save you money if you make your own meal at home instead of dining out?

Do you always pay extra to your Telco provider because you always exceed your data allowance?

Why not upgrade monthly plan?

Do what you need to do to minimise your spending habits. Remember, there’s a difference between Wants and Needs.

Make extra payments

Repaying the minimum required payment on your credit card will take years to repay and interest charges will top up to your debt.

If you pay more than $20 – $30 per month makes a difference when accumulated.

You may also choose to accelerate the debt off to save you hundreds or thousands of interests, terms may vary for every credit card provider.

Don’t Use Your Cards

This is the easiest way to eliminate your credit card debt.

Stop swiping until it’s all paid off. Leave the cards at home and always pay cash.

People tend to spend double when they’re paying with a credit card as opposed to cash payment. If you still use your credit cards whilst trying your best to pay your debt off, then you’re putting yourself into the burden.

Understand that credit card is not free money.

Get help if you need

At Credit Fix Solutions, we have expert advisers who can provide you with professional credit score repair services, build your credit, minimise your debt, and negotiate with collection agencies.

We will act as your advocate, meaning that all communications will come to our office on your behalf, leaving you free to get on with your life whilst we deal with the negotiations.

If you require assistance to negotiate any unpaid debts, contact us now!

No Result No Fee!

Call us on 1300 436 569! Email us at [email protected] or check out more articles at https://www.creditfixsolutions.co.nz/